Introduction:

The launch of the Jan Samarth Portal on 6 June 2022 transformed this landscape. It directly bridges the gap between commercial lenders and beneficiaries by replacing fragmented processes with an integrated, technology-driven automated rules engine. The portal lowers transaction costs, enforces transparency, and drives credit delivery to underserved areas.

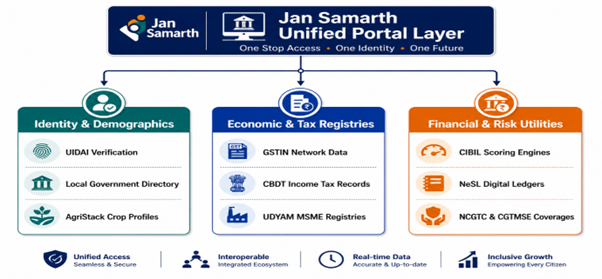

Architectural Layout of the Jan Samarth Ecosystem

The portal functions as an interoperable Digital Public Infrastructure (DPI) layer, executing real-time data validation by checking across prominent government and tax databases:

Real-Time Data Integration Nodes

-

- Identity & Verification: Integrates with the Unique Identification Authority of India (UIDAI) placeholder framework, the Local Government Directory (LGD), and LOKoS to verify location and applicant metrics instantly.

- Sectoral Repositories: Connects with AgriStack for agricultural mappings, the Startup Portal of DPIIT for tech ventures, and UDYAM for verified MSME classifications.

- Fiscal & Revenue Trails: Links directly with the Central Board of Direct Taxes (CBDT) and the Goods and Services Tax (GST) systems to pull verified income and corporate tax invoice histories.

- Risk & Trust Facilities: Leverages National E-Governance Services Ltd. (NeSL), NSDL, credit information bureaus (CIBIL), and credit guarantee trusts like NCGTC and CGTMSE to evaluate risk metrics immediately.

Matrix of Loan Categories and Integrated Central Schemes

The portal structures 16 statutory credit-linked schemes across 8 distinct economic categories to simplify onboarding:

| S.No | Loan Category | Mapped Central Government Schemes |

|---|---|---|

| 1 | Credit Guarantee Coverage | Emergency Credit Line Guarantee Scheme 5.0 (ECLGS) |

| 2 | e-NWR Financing | e-Kisan Upaj Nidhi (EKUN) for electronic warehouse receipts |

| 3 | Home Loan | Home Loan for EWS, LIG, and MIG in Urban Areas (HL-U) |

| 4 | Agri Loan (Kisan Credit Card) | Kisan Credit Card (KCC) & Kisan Credit Card–Fisheries (KCCFIM) |

| 5 | Renewable Energy | Roof Top Solar Installation Financing (SOLAR) |

| 6 | Agri Infrastructure Loan | Agri Clinics and Agri Business Centers (ACABC); Agriculture Infrastructure Fund (AIF) |

| 7 | Business Activity Loan | PMEGP; Weaver Mudra Scheme (WMS); PMMY (Mudra); PM SVANidhi; NAMASTE; Startup Loans (START); Credit Card for Micro Enterprises (CCME) |

| 8 | Livelihood Loan | Deendayal Antyodaya Yojana–National Rural Livelihoods Mission (DAY-NRLM) |

End-to-End Digital Lending Journey

The workflow minimizes documentation requirements and speeds up credit underwriting through an interactive, completely paperless framework:

![]()

1. Intelligent Compatibility Matching: The user responds to a brief series of digital questions, and the platform automatically suggests the best-suited government scheme.

2. Automated Data Population: Advanced APIs securely fetch details from integrated databases, eliminating manual data-entry errors.

3. Inbuilt Automated Business Rule Engine: Analyzes data to provide instant in-principle sanctions, routing the application and validated dossiers directly to the applicant’s chosen Member Lending Institution branch.

4. Real-Time Stage Updating: Keeps applicants fully updated at every processing step via mobile app and web alerts, eliminating the need for physical bank branch visits.

5. Assisted Delivery Mode: Provides a dedicated assisted portal mode for Bank Business Correspondents (BCs) and assisted partners to register digitally excluded rural applicants.

Challenges:

-

- First-Mile Digital Literacy Gaps: While the platform operates seamlessly across 8 languages, rural smallholders often lack the digital literacy to navigate multi-step database consents independently, making them dependent on third-party intermediaries or Business Correspondents.

-

- Underutilization of Co-Lending Options: Out of the 269 onboarded lenders, District Central Cooperative Banks (180 DCCBs) often face local legacy technology mismatches when connecting their backend systems with the portal’s high-speed API rule engine.

- Data Standardization Across States: While tax records like GST are centralized, checking land records via AgriStack interfaces faces hurdles in regions where digital land registration and cadastral mapping remain incomplete.

Way Forward:

-

- Transition to Advanced AI Translation (Bhashini): Upgrading the portal’s language rails by integrating Banking BHASHINI to provide conversational, voice-based loan matching across all 22 scheduled Indian languages.

- Deploying Pre-Approved Micro-Credit for Street Vendors: Combining PM SVANidhi data with alternative transactional data on the Unified Lending Interface (ULI) to grant instant, algorithmically backed loan renewals.

- API Harmonization for Cooperative Banking: Funding targeted technological upgrades across DCCBs and Regional Rural Banks to ensure uniform processing speeds across all member institutions.

- Expanding Credit Guarantee Automation: Linking the application flow with automated escrow and credit risk modeling to further lower collateral thresholds for first-time startup applicants.

Conclusion

Over its four-year journey, the Jan Samarth Portal has evolved from a standard aggregative portal into an intelligent, data-driven engine for financial empowerment. By successfully processing over ₹3 lakh crore in digital applications, it demonstrates the power of combining open-architecture APIs with targeted social welfare goals.

Spread the Word