Introduction

India’s macroeconomic strategy has pivoted toward integrating its domestic capital markets with global financial systems. By rewriting the taxation landscape and broadening the open-access investment window. The state seeks to diversify its investor base, smooth out the domestic sovereign yield curve, lower government borrowing costs, and significantly expand the transmission of monetary policy across the financial spectrum.

Institutional Architecture

To systematically parse the fixed-income terrain, the following market components are defined:

-

- Government Securities (G-Secs): Tradable sovereign debt contracts issued by the Central or State governments to manage fiscal deficits, adjust commercial banking liquidity, and fund public utility assets.

- Foreign Portfolio Investment (FPI) vs. FII: FPI represents passive cross-border allocations in shares, municipal/state bonds, or mutual funds without direct corporate governance or board controls. Foreign Institutional Investment (FII) is an institutional sub-tier of FPI (e.g., pension assets, sovereign wealth funds, hedge funds) that deploys large pooled capital reserves driven by active research models.

- Bank for International Settlements (BIS): An elite intergovernmental financial infrastructure owned by central banks that serves as an institutional forum to foster global monetary stability and acts as a specialized asset manager for central banks.

The Taxation Metamorphosis

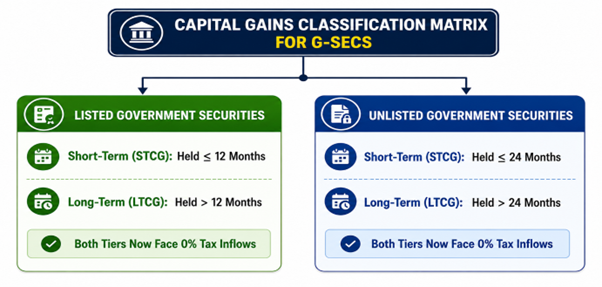

The structural tax changes introduced via the Income-tax (Amendment) Ordinance, 2026 eliminate the compliance friction that historically dented net yields for foreign funds:

1. The Pre-Reform Tax Matrix: Previously governed under Section 210 of the Income-tax Act, 2025, foreign funds faced direct deductions that reduced their globally competitive internal rates of return (IRR):

-

- Interest Income: Taxed at a flat 20% on coupon payouts.

- Short-Term Capital Gains (STCG): Subject to a steep 30% deduction on trading turnovers.

- Long-Term Capital Gains (LTCG): Taxed at a fixed 5% rate.

2. The New Absolute Exemption Regime: Applies universally to all interest income and capital gains generated from the sale, transfer, exchange, or redemption of G-Secs realized on or after 1 April 2026.

G-Sec Infrastructure & Core Architectural Reforms: Foreign institutional capital routes into sovereign paper have been radically simplified:

1. Structural Expansion of the Fully Accessible Route (FAR): Unlike the standard General Route, which contains regulatory holding limits, FAR functions as an unrestricted, open-access channel for select securities. To capture long-duration institutional capital (such as global pension assets and insurance funds), the government expanded FAR to include:

-

- New sovereign issuances with 15-year, 30-year, and 40-year tenors.

- Sovereign Green Bonds (SGrBs) issued within these FAR-eligible tenors, advancing India’s green finance infrastructure.

2. Regulatory Easing of the General Route: To minimize operational drag and ease portfolio rebalancing, the Reserve Bank of India has eliminated three major restrictions under the General Route: the Short-term investment limit, the Concentration limit, and the Security-wise investment ceiling.

3. Streamlining the Macro-Prudential Framework: The structural categories for ‘General’ and ‘Long-Term’ FPI limits have been merged into a simplified single investment limit. However, to preserve national monetary sovereignty, the overarching macro caps remain anchored at:

-

- 6% of the total outstanding stock of Central Government Securities.

- 2% of the total outstanding stock of State Government Securities (SGSs).

Structural Exposure Analysis

The configuration of FPI allocations across sovereign debt paths as of 12 May 2026 reflects the immediate popularity of unrestricted access rails:

| Investment Channel | FPI Holdings (₹) | Total Outstanding Stock (₹) | Active FPI Percentage Share |

| General Route | ₹54,091 crore | ₹64.78 lakh crore | 0.83% |

| Fully Accessible Route (FAR) | ₹3,21,080 crore | ₹47.63 lakh crore | 6.74% |

| Aggregate Total | ₹3,75,171 crore | ₹112.42 lakh crore | 3.34% |

Challenges

-

- The Hindu editorial analysis cautions that expanding foreign debt footprints increases vulnerability to global financial shifts. While 0% tax regimes attract stable capital, a sudden change in interest rates by the US Federal Reserve can still trigger rapid FPI capital outflows. This puts sudden pressure on the rupee’s exchange rate and complicates the RBI’s domestic liquidity management.

- The Indian Express highlights that while the FPI limit for State Government Securities (SGSs) stands at a generous 2%, actual foreign utilization remains negligible. FPIs heavily favor highly liquid, central FAR-eligible papers, leaving state-level development loans out of the global investment loop due to fragmented secondary market structures.

- Policy briefs from the Observer Research Foundation (ORF) emphasize that as Indian bonds achieve higher weightages in major global indices (like JPMorgan and Bloomberg-Barely), the incoming capital is primarily passive index-tracking funds. This type of capital is highly automated and sensitive to global indexing parameters, rather than India’s intrinsic domestic fiscal health. This systemic reliance demands flawless, glitch-free domestic settlement infrastructures like Euroclear-style connections.

Way Forward

-

- Exploring ways to leverage the Unified Lending Interface (ULI) data rails to let primary dealers use alternative institutional data to optimize real-time settlement margins.

- Selecting highly liquid state development bonds from transparently governed states to enter the Fully Accessible Route, actively diversifying foreign allocations beyond central papers.

- Creating customized, tax-exempt currency and interest-rate derivative desks at the GIFT International Financial Services Centre to allow FPIs to insulate their long-duration 40-year investments against exchange-rate volatility.

- Setting up an automated digital tax clearance vault under the NSDL/CDSL network to ensure zero delays in executing the 2026 Ordinance guidelines for global custodians.

Conclusion

The 2026 sovereign debt market transformations mark a significant milestone in India’s financial evolution, moving away from closed, defensive capital tracking toward a mature, globally integrated marketplace. By matching absolute tax exemptions with long-duration 40-year FAR asset extensions and green bond pipelines, the state lowers the structural costs of national deficit financing.

Spread the Word