THE CONTEXT: As economic activity started showing signs of picking up in the second year of the pandemic, the global economy faced the fresh challenge of rising global inflation. COVID-19 related stimulus spending in major economies along with pent-up demand boosting consumer spending pushed inflation up in many advanced and emerging economies. The surge in energy, food, non-food commodities, and input prices, supply constraints, disruption of global supply chains, and rising freight costs across the globe stoked global inflation during the year.

RETAIL INFLATION

The retail inflation, as measured by Consumer Price Index-Combined (CPI-C) moderates to 5.2% in 2021-22 (April-December) from 6.6% in the corresponding period of 2020-21. The Survey also says effective supply-side management kept prices of most essential commodities under control during the year.

DOMESTIC INFLATION

Compared to many Emerging Markets and Developing Economies (EMDEs) and advanced economies, the Survey finds that Consumer Price Index – Combined (CPI-C) inflation in India has remained range-bound in the recent months, touching 5.2% in December 2021. This was possible largely because of the proactive steps taken by the Government for effective supply management.

GLOBAL INFLATION

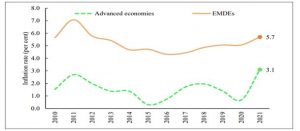

- In 2021, inflation picked up globally as economic activity revived with the opening up of economies. Inflation surged from 0.7 % in 2020 to around 3.1 % in 2021 in the advanced economies. For instance, inflation in the USA touched 7.0 % in December 2021, the highest since 1982. In the UK, it hit a nearly 30 years high of 5.4% in December 2021. Among emerging markets, Brazil witnessed inflation of 10.1% in December 2021 and Turkey also saw double-digit inflation touching 36.1%. Argentina has been experiencing inflation rates above 50% during the last 6 months.

RECENT TRENDS IN RETAIL INFLATION

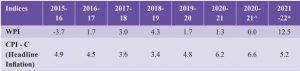

- Retail inflation, well within the target limits of 2% to 6%, declined to 5.2% as against 6.6% during April – December 2020-21. The Survey states that this was largely attributed due to the easing of food inflation. Food inflation, as measured by the Consumer Food Price Index (CFPI), averaged at a low of 2.9% in 2021-22 (April-December) as against 9.1% in the corresponding period last year.

- A “refined” Core inflation has been constructed to exclude the volatile fuel items. The items of “petrol for vehicle” and “diesel for vehicle” and “lubricants & other fuels for vehicles”, in addition to “food and beverages” and “fuel and light” have been excluded from headline retail inflation. Since June 2020, refined core inflation has been much below the conventional core inflation, indicating the impact of inflation in fuel items in the “conventional” core inflation measure.

DRIVERS OF RETAIL INFLATION

- Major drivers of retail inflation have been the “miscellaneous” and “fuel & light” groups. Contribution of miscellaneous increased to 35% in 2021-22 (April – December) from 26.8% in 2020-21 (April – December). According to the Survey, within the miscellaneous group, a subgroup of “transport and Communication” contributed the most, followed by “health”. On the other hand, the contribution of food & beverages declined from 59% to 31.9%.

“FUEL & LIGHT” AND “TRANSPORT & COMMUNICATION”

- Inflation in the above two groups for the period of 2021-22 (April – December) has been largely due to the high international crude oil, petroleum product prices, and higher taxes.

MISCELLANEOUS

- Apart from transport & communication; “clothing and footwear” inflation also saw a rising trend during the current financial year possibly indicating higher production and input costs (including imported inputs) as well as due to revival of consumer demand.

FOOD AND BEVERAGES

- “Oils and fats” contributed around 60% of “food and beverages” inflation despite having a weight of only 7.8% in the group. The demand for edible oils is largely met through imports (60%) and fluctuations in international prices have been responsible for the high inflation in this subgroup. Though India’s imports of edible oils have been the lowest in the last six years, in terms of value, it has increased by 63.5% in 2020-21 as compared to 2019-20.

- Inflation in pulses declined to 2.4% in December 2021from 16.4% in 2020-21.With an increase in area sown for Kharif pulses to a new high of 142.4 lakh hectares (as of 1stOctober 2021) pulses inflation is on a downward trajectory.

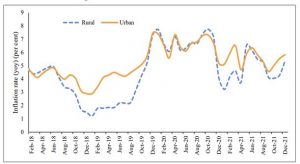

RURAL-URBAN INFLATION DIFFERENTIAL

- The gap between rural and urban CPI inflation declined in 2020 as compared to the higher gaps witnessed from July 2018 to December 2019. The factor largely responsible for divergence, for brief periods, is the component of food and beverages.

TRENDS IN WHOLESALE PRICE INDEX-BASED INFLATION

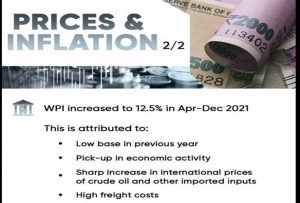

- WPI inflation has shown an increasing trend and has remained high during the current financial year touching 12.5% during 2021-22 (April – December). The Survey describes that part of the high inflation could be because of a low base in the previous year as WPI inflation has been benign during 2020-21.

- Crude petroleum & natural gas subgroup under WPI has witnessed very high inflation and stood at 55.7% in December 2021. Within manufactured food products, edible oils were a major contributor.

DIVERGENCE BETWEEN WPI AND CPI-BASED INFLATION RATES

- The Survey attributes a host of factors for the divergence witnessed between the two indices. Some of them, amongst others, include the variations due to base effect, the conceptual difference in their purpose and design, the price behavior of the different components of the two indices, and lagging demand pick up. The Survey states that with the gradual waning of base effect in WPI its divergence in WPI and CPI inflation is expected to narrow down.

HOUSING PRICES

- The residential housing sector was also affected by COVID-19 induced restrictions through both supply and demand channels.

- Amidst initial COVID-19 restrictions, not only did the construction of new houses slow down but the launch of new housing projects also got delayed. With the loss of income, uncertainty about future income, and stay-at-home orders, home buyers delayed their housing purchases.

- During the second COVID-19 wave (April-June, 2021), transactions of housing properties were once again impacted adversely, but not as much as it was seen during the first COVID-19 wave (April-June, 2020).

PHARMACEUTICAL PRICING

- Several steps have been taken to ensure the affordability of drugs and medical devices. Ceiling prices for 355 medicines and 886 formulations were fixed for medicines under the National List of Essential Medicines, 2015 until 31 December 2021.

- Retail prices for approximately 1798 formulations were fixed under DPCO, 2013 till 31 December 2021.

- During the recent years, exercising extraordinary powers under DPCO, 2013 in the public interest, prices of coronary stents and knee implants have also been fixed.

- NPPA also capped the trade margin up to 30 percent on selected 42 anti-cancer non-schedule medicine on a pilot basis in February 2019.

LONG TERM PERSPECTIVE

- Given the importance of supply-side factors in having a predominance in the determination of inflation in India, certain long-term policies are likely to help. This includes changing production patterns which would lead to diversification of production of crops, calibrated import policy to address uncertainty, and increased focus on transportation and storage infrastructure for perishable commodities.

- Better storage and supply chain management is required to ensure availability in lean season and reduced wastages of horticulture and other perishable essential commodities to reduce the seasonal spikes in prices for consumers, glut for the farmers in times of good harvests due to lack of marketing infrastructure, resulting in distress sales.

- Effective utilization of the Agriculture Infrastructure Fund for investment in viable projects for post-harvest management infrastructure for perishable commodities can help improve agriculture infrastructure in the country.

- Schemes like Operation Green and Kisan Rail need to be exploited further to protect the interests of the farmers as well as the consumers.

HIGHLIGHTS

- The average headline CPI-Combined inflation moderated to 5.2 percent in 2021-22 (April-December) from 6.6 percent in the corresponding period of 2020-21.

- The decline in retail inflation was led by the easing of food inflation.

- Food inflation averaged at a low of 2.9 percent in 2021-22 (April to December) as against 9.1 percent in the corresponding period last year.

- Effective supply-side management kept prices of most essential commodities under control during the year.

- Proactive measures were taken to contain the price rise in pulses and edible oils.

- Reduction in central excise and subsequent cuts in Value Added Tax by most States helped ease petrol and diesel prices.

- Wholesale inflation based on the Wholesale Price Index (WPI) rose to 12.5 percent during 2021-22 (April to December).

- This has been attributed to:

- Low base in the previous year,

- Pick-up in economic activity,

- Sharp increase in international prices of crude oil and other imported inputs, and

- High freight costs.

- Divergence between CPI-C and WPI Inflation:

- The divergence peaked to 9.6 percentage points in May 2020.

- However, this year there was a reversal in divergence with retail inflation falling below wholesale inflation by 8.0 percentage points in December 2021.

- This divergence can be explained by factors such as:

- Variations due to base effect,

- Difference in scope and coverage of the two indices,

- Price collections,

- Items covered,

- Difference in commodity weights, and

- WPI being more sensitive to cost-push inflation led by imported inputs.

Spread the Word