THE CONTEXT– The first International Energy Association (IEA) Summit on Critical Minerals and Clean Energy was held at Paris, France on September 28, 2023. At the heart of its agenda remained the discussions on the challenges and opportunities in meeting the rising demand for minerals required for clean energy technologies.

As economic transformations accelerate, securing access to these materials will both impact and help shape geopolitics in the years to come. This article delves into the developments concerning energy geopolitics from multiple dimensions and analyses the options available to India in securing its national interests.

WHAT IS GEOPOLITICS?

The term “Geopolitics” can be broadly understood as the influence of geography and economics on the power status of a country and its relationships as well as decisions in the bilateral and/or multilateral arena.

Geopolitics seeks to study the effects of the Earth’s geography (human and physical) on politics and international relations.

It is concerned with questions of influence and power over space and territory. It uses geographical frames to make sense of world affairs.

WHY IS ENERGY AN IMPORTANT PART OF GEOPOLITICS?

- Since the industrial revolution, the geopolitics of energy- who supplies it and securing ways for reliable access to those resources- has been influencing the geoeconomics of the nations and the world as a whole.

- Energy is a fundamental resource that drives the global economy and shapes international relations which makes it a crucial component of geopolitics.

- The availability, accessibility, and affordability of energy resources can have significant impacts on a country’s economic growth, political stability, and national security.

- Energy resources are finite and unevenly distributed across the world, which has led to competition among countries for access to these resources. This competition has often resulted in geopolitical tensions, conflicts, and even wars. For instance: Gulf war of 1990s. One of the major factors behind Iran’s annexation of Kuwait was its interest in accessing the rich oil reserves of the latter.

- Heartland Theory (Halford Mackinder) and Rimland Theory (Nicholas Spykman) concerning geopolitics highlighted the importance of gaining control over resource-rich regions if a country was to establish and expand influence/hegemony in the world. In this context, countries rich in oil, gas and other energy resources enjoy an edge over resource-strained countries in terms of power and influence.

- For any country to secure its national interests such as energy security and industrial development, having a reliable supply chain of those energy resources is necessary which dictates the decisions of the country in bilateral/multilateral relationships.

CONTEMPORARY DEVELOPMENTS INVOLVING ENERGY AS PART OF GEOPOLITICS

Presenting a region-wise discussion on the geopolitics of energy-

EUROPE AND BLACK SEA REGION

Impacts of Russia-Ukraine war: The energy dynamics of the world have been shaped drastically and multidimensionally because of the Russia-Ukraine war-

- Weaponisation of energy by Russia- It was no accident that Russia invaded Ukraine in February 2022, when it is the coldest and European demand for gas for heating buildings is the highest. Russia cut gas flows to the EU by around 80% in 2022, leaving the bloc with a significant shortfall in its energy mix, and a pressing need to find energy alternatives from other places.

- Russia cut supplies to Europe in retaliation for western sanctions over its invasion of Ukraine. This resulted into surge in the prices of electricity, often linked to the price of gas. And that has pushed energy security to the top of the political agenda.

- Attack on Nord Stream pipelines- Russia has been blamed for blast of the Nord Stream pipeline in Baltic Sea which supplied gas from Russia to the European nations like Germany. Extensive damage to Nord Stream 1 and 2 in the Danish exclusive economic zone has been reported in the wake of Russia-Ukraine war in 2022. This has raised energy security challenges for the European countries.

- Discounted Russian oil and geopolitics- The energy resource-rich Russia took advantage of the war to increase its revenue and geopolitical influence through the sale of discounted oil to countries like India and China.

However, under the pressure from Western sanctions on crude oil, Russia in February 2023 decided to cut its production and supply of crude oil. Such disruptions in the energy supply chains and heavy dependence of nations on oil/gas imports leave them in a vulnerable situation.

- Energy resources in the Black Sea- The Russia-Ukraine war which begun as Russian response to Ukraine’s intent to become a member of NATO, also has energy geopolitics as its core. Given the huge potential reserves of oil and natural gas in the Black Sea region, Russia intends to secure its access to the energy resources.

ARCTIC REGION

In a changing Arctic, this potentially resource-rich region could become another venue for geopolitical tensions. Russia has launched an ambitious plan to remilitarize the Arctic. Specifically, Russia is searching for evidence to prove its territorial claims to additional portions of the Arctic, so that it can move its Arctic borderline — which currently measures over 14,000 miles in length — further north.

- Climate Change and new energy resources- The rapid loss of Arctic Sea ice at a much fast rate than the rest of the world has exposed new lands with high potential for energy resources like oil, natural gas, shale gas and methane hydrates. The United States Geological Survey estimates that the Arctic contains approximately 13% of the world’s undiscovered oil resources and about 30% of its undiscovered natural gas resources.

- Race to control the Arctic energy resources- A race for access to the new potential energy reserves in the Arctic has been shaping the geopolitical agenda and moves of countries like the USA, Russia, China etc. Each party wishes to gain control over these energy resources that would translate into increased geopolitical influence of countries in the future.

- New trade routes for energy- The thawing ice cover in the Arctic is opening new trade routes which are likely to be used as alternative energy trade routes between the countries in the Northern Hemisphere. Control of these routes could bring significant advantages to countries and corporations looking for a competitive edge.

SOUTH CHINA SEA (SCS)

Disputes between China and Southeast Asian countries:

- Since the exploration in the early 20th century, more than 10 billion tonnes of Cenozoic oil and gas fields have been discovered, making the SCS region one of the giant oil and gas areas.

- Estimates by the US Geological Survey and others indicate that about 60%-70% of the region’s hydrocarbon resources are gas.

- Optimistic Chinese estimates of the region’s oil potential indicate as high as 213 billion barrels of hydrocarbons which are untapped. This figure is comparable with any high-value hydrocarbon producing region of the world, including the Persian Gulf region.

- Energy security and hegemony in the international energy trade has been one of the factors behind increasing Chinese muscular power in the SCS region. E.g. growing standoffs between the Philippines and China.

GULF REGION

- In the early twentieth century, the switch from coal to oil formed the basis to a century of geopolitical upheaval in the Middle East.

- Gulf war (1990s)- One of the major factors behind Iran’s annexation of Kuwait was its interest in accessing the rich oil reserves of the latter.

- Cartelisation- The control of OPEC and OPEC+ over the production of oil and the decision of its members to cut production and supply of crude oil has always been a cause of worry for the countries that remain dependent on imports of oil to meet their growing energy demands. The production cuts lead to hike in the oil prices.

- Ongoing Israel-Hamas conflict- Iran, a major oil producer, backs the Hamas group which is at war with Israel. As the Hamas attack on Israel intensified, experts have expressed serious concerns on its impact on oil prices, gold prices, inflation and eventually the economy.

- India-Middle East-Europe Corridor- This new counter-BRI initiative, launched at the sidelines of the recent G20 Summit (2023), has energy security and trade among its core objectives. Such regional projects shape the dynamics of international trade in energy. The IMEC will involve rail connectivity, shipping lines, high-speed data cables, and energy pipelines.

o The volatile situation in the Middle East with the ongoing Israel-Palestine conflict could hit the corridor plans.

o This ambitious project aims to create a seamless trade route connecting India, the UAE, Saudi Arabia, Jordan, Israel and Europe. The corridor spans diverse nations with varying political dynamics, interests and previous tensions.

CLIMATE CHANGE AND GEOPOLITICS OF RENEWABLE ENERGY:

RENEWABLE ENERGY

While the global community has ramped its efforts towards green transition to decarbonise economy and achieve climate goals at the earliest, the geopolitics around renewable energy and just transition has been a big challenge, especially for developing countries and LDCs.

- CBDR and Climate Finance- Compelled by the limited financial resources, the developing nations and LDCs seek increased financial assistance in the form of Climate Finance to facilitate shift towards renewable energy and to reduce share of fossil fuels in the energy mix. However, the promise of raising $100 billion as climate finance by the developed countries has remained unfulfilled.

- Technological Supremacy of West- The slower development of renewable energy sources (solar, wind, bio-energy, etc.) and higher costs of renewable energy are attributed to the lack of technology at the disposal of the Third World countries. The West having developed advanced technology for exploitation of green hydrogen, waste-to-energy and hybrid renewable energy, has been reluctant to share their technical know-how with the less developed nation, thus, establishing their supremacy and using it as a weapon of geopolitics.

- Critical Minerals Race- From 2017 to 2022, green energy projects alone boosted demand for lithium by roughly 200 percent, cobalt by 70 percent and nickel by 40 percent.

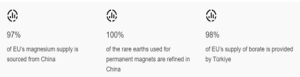

- Chinese monopoly- The uneven geographical distribution of critical minerals and near-monopoly of China in their production, refining and exports raise apprehensions regarding reliable, efficient supply chain of critical minerals.

Such dependencies create a high risk of supply disruptions and increase the Union’s vulnerability and security risks.

According to the International Energy Agency (IEA), China is home to about 35% of the world’s nickel, 58% of lithium, 65% of cobalt, and 87% of rare earth elements (REE) i.e. cerium, lanthanum, praseodymium etc.

- The European Critical Raw Materials Act was voted on in the European Parliament during the September 11-14, 2023, seeks to diversify its supply chain for reliable supply of critical minerals. Most importantly, it aims to reduce its heavy dependence on China.

- Deep sea mining race- In an attempt of diversify the supply chains and explore new regions for untapped critical minerals (in the seabed), countries such as Australia, India, USA have joined hands to counter the Chinese monopoly. The deep-sea mining for polymetallic nodules and other critical minerals by countries has surged, and in response, the reports of EEZ encroachments have also witnessed a rise.

- Elitist nature of the Minerals Security Partnership- The MSP is elitist in its very idea of formation and induction of members. Countries like Indonesia, Vietnam, the Democratic Republic of Congo, which have abundant reserves of critical minerals are not part of this strategic grouping formed by US.

MSP is a strategic grouping of 13 member states including Australia, Canada, Finland, France, Germany, Japan, the Republic of Korea, Sweden, the United Kingdom, US, the European Union, Italy and India.

CARBON BORDER ADJUSTMENT MECHANISM (CBAM)

The European Union (EU) has launched a carbon border tax on carbon intensive imports of products such as cement and fertilizer with the intent to prevent carbon leakage and incentivise green manufacturing.

- Challenges for developing countries like India- India and other developing countries which are trade partners of the EU raise concerns regarding the discriminatory nature of this carbon levy, given the fact that fossil fuels like coal, oil and gas still contribute nearly 60% of India’s energy mix.

- It is a challenge for India to make sudden transition towards renewable energy generation to drive the green manufacturing. Thus, the EU’s CBAM is touted as a geopolitical tactic used by the EU to further its interests at the stake of the interests of the less-competitive countries.

HOW IS INDIA ENSURING ENERGY SECURITY AND PROTECTING ITS INTERESTS THROUGH GEOPOLITICS?

As per the ‘2023 World Energy Outlook’ published by the OPEC, India’s primary energy demand will nearly more than double to 38.5 million barrels of oil equivalent per day (mboe/d) in 2045. India’s energy demand will also reach 10 per cent of global demand, up from 6.6 per cent currently.

The surging energy demands in the country and climate action have influenced the foreign policy of India in a bid to secure its national interests and ensure energy security:

- Discounted Russian oil – Taking advantage of the discounts offered by Russia on crude oil in the aftermath of Russia-Ukraine war, India began purchasing Russian oil so as to diversify its trade partners in the field of energy resources. Russia has emerged as the largest oil importer of India, accounting for about 40% of India’s crude imports.

- India and Russia recently discussed the possibility of exploring new transport corridors like the Northern Sea Route (NSR) and the Eastern Maritime Corridor (EMC) between Vladivostok and Chennai and both sides also agreed that Indian seafarers will be trained on Polar and Arctic waters at the Russian Maritime Training Institute in Vladivostok, which is equipped with simulators.

- India invested to develop Chabahar port in Iran. This will help bypass Pakistan and have access to oil and mineral rich Iran, Afghanistan and Central Asian countries.

- International Solar Alliance- The International Solar Alliance (ISA) founded by India in 2015, is an action-oriented, member-driven, collaborative platform for increased deployment of solar energy technologies as a means for bringing energy access, ensuring energy security, and driving energy transition in its member countries.

- Global Biofuels Alliance (launched on the sidelines of G20 Summit in New Delhi 2023)- India as a founder member of GBA, has been focussing on scaling up the share of biofuels through sharing of technical know-how and encouraging investments in the R&D in waste-to-energy. The efforts by India to ramp up biofuels in energy basket of India aims to scale down the share of fossil fuels in energy mix.

- Green Hydrogen Alliances- Recently, India and Saudi Arabia have signed a Memorandum of Understanding (MoU) for the development of a green hydrogen supply chain which seeks to expand the cooperation among the two nations in the co-production of green hydrogen and the creation of secure, reliable, and resilient supply chains for materials used in green and clean hydrogen production and renewable energy.

CHALLENGES FOR INDIA

HIGH IMPORT-DEPENDENCE FOR CRUDE OIL

- India’s oil import dependency was 84.4 per cent in 2020-21, 85 per cent in 2019-20, and 83.8 per cent in 2018-19.

- The share of Persian Gulf countries in India’s crude imports has remained at around 60% over the last 15 years.

- Also, Russia has emerged as the largest oil sourcing country for India in 2023, which has its own set of challenges in the wake of potential supply chain disruptions and growing bonhomie between Russia and China. The geodynamic equations and sanctions by the West on Russia are potential threats to energy security interests of India.

NUCLEAR SUPPLIERS GROUP

- The nuclear energy generation in India is hindered by the limited domestic reserves of uranium (about 2% of the world’s total uranium reserves) and reliance on imports of nuclear fuel and nuclear technology.

- India’s entry into the Nuclear Suppliers Group is stonewalled by China which hurts the energy interests of India. China plays the Pakistan card and NPT entry as conditions for India to become a member of the NSG. India has been seeking NSG membership to gain access to foreign-sourced nuclear material and technology.

LACK OF DOMESTIC RESERVES OF CRITICAL MINERALS

- India lacks reserves of critical minerals such as lithium and cobalt.

- The complex supply chains, disruptions sue to political instability in Africa, Chinese dominance in production and processing of about 90% of critical minerals and heavy dependence of India for critical minerals are among the major challenges facing industrial development and green transition in the country.

- Countries such as Democratic Republic of Congo lead in the reserves of cobalt (about 70% of total reserves).

- Russia is a significant producer of nickel, palladium, titanium sponge, & scandium and Ukraine is a major producer of titanium; the Russia-Ukraine war has disrupted the supply chains.

HIGH COMPARATIVE COSTS OF RENEWABLE ENERGY

- While renewable energy sources may appear to be cheaper, there are some hidden and indirect costs that make them far less financially attractive.

- Given the intermittent nature of sources like solar and wind, energy storage solutions such as batteries, become crucial.

- While the initial costs of renewable installations might seem competitive, the associated storage costs can be significant, especially when we factor in the lifespan and efficiency of current battery technologies. This is particularly relevant when comparing the continuous power generation capabilities of fossil fuel plants to the on-and-off nature of renewables.

2070 CARBON-NEUTRALITY AS CHALLENGE

- There are numerous hurdles in India’s target for carbon-neutrality by 2070.

- One, it would require about $10 trillion investment and given the constraints in climate finance mobilisation, it seems an arduous task.

- Secondly, phasing out coal completely is difficult, given the requirements of industries and slow progress in addition of renewable energy. Also, the intermittent nature of renewables makes coal a viable option.

- It also requires innovation and collaborations in the desired technologies to meet the target in the long run.

THE WAY FORWARD

India must secure its energy interests through the following measures:

- Strategic Petroleum Reserves- All oil importing member countries of the International Energy Agency (IEA) have an obligation to hold emergency oil stocks equivalent to at least 90 days of net oil imports. India with the help of imported oil has been building its strategic petroleum reserves at Vishakhapatnam, Mangalore and Padur. India should also consider having strategic reserves of coal as well as natural gas.

- Strategic autonomy- India must proactively exercise its strategic autonomy in maintenance of bilateral and multilateral relations to secure the national interests of the country in energy sector. Therefore, India must maintain its healthy relations with the Middle East, Russia as well as the USA for diversification of risks associated with suppliant chain management of energy resources and critical minerals supply.

The 3-year India-Australia Critical Minerals Investment Partnership and purchase of discounted Russian oil in this context are the right measures.

- Critical Minerals Partnerships- India’s membership in the Minerals Security Partnership, state-owned joint venture KABIL’s agreement with Argentina to tap the critical minerals are the much-needed initiatives towards reliable and efficient critical minerals supply chain. Such opportunities must be leveraged well by the Indian government and investors.

- Commercial mining of critical minerals- The rising demand of critical minerals for green energy transition and inadequate, slow progress in exploration and production of potential domestic reserves of critical minerals have driven India’s amendments in the Minerals and Mines (Development and Regulation) Act 1957, to boost commercial mining of select critical minerals in the country. Private participation in mining of critical minerals with increased investments in the R&D is imperative.

- Deep Ocean exploration- India must ensure robust implementation of the crucial policies such as Deep Ocean Mission, O-SMART and Samudrayaan Mission (Matsya 6000) to explore, tap and exploit the polymetallic nodules and other energy resources to fulfil the burgeoning energy demands of the country.

- Geospatial Energy Mapping- The Geospatial Energy Map of India launched by IRSO and Niti Aayog (2021) attempts to identify and locate all primary and secondary sources of energy and their transportation/transmission networks to provide a comprehensive view of energy production and distribution in a country. It should be used effectively by the private sector and other stakeholders in research and development of energy resources.

THE CONCLUSION- Energy and geopolitics are intertwined. With new discoveries of energy resources (shale gas in the USA, lithium reserves in India, etc.) and innovations in associated technologies, the energy sector dominates in the negotiations and agreements between the nations and will continue to have its influence on foreign policy of the nations in future as well. India must carefully weigh its options and make the best out of its deals, agreements at the bilateral, regional, or multilateral forums.

MAINS PRACTICE QUESTIONS:

Q. Climate change is changing the energy geopolitics globally, with significant implications for India. Comment.

Q. The melting of the Arctic has been shaping the energy dynamics of the world. Discuss in the context of importance of Arctic region for India.

Q. The Russia-Ukraine war has dramatically transformed the energy dynamics of the world. In this context, comment on India’s approach to fulfil its national interest.

Spread the Word