A. Direct Tax

-

- It is a type of tax in which incidence and burden (or impact) of tax falls on the same person or entity.

- The burden cannot be shifted to another person.

- Basically, tax is levied and collected from the same person.

- It involves complex calculations as many exemptions and slab rates are applicable.

- An increase in direct tax rate may help in combating inflation as disposable income reduces which may lead to lower demand of goods and services.

Important Direct Taxes

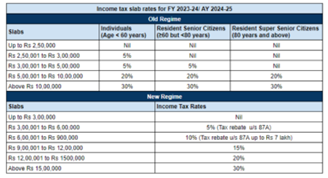

1. Personal income Tax (or Income Tax)

-

- It is levied on individual person, Hindu Undivided Family (HUF) and proprietorship firm.

- There are various slabs of income tax rate which is dependent on the total income of the person under assessment.

- While calculating personal income tax, all types of incomes are included which include salary and wages, dividend, rental income, interest income, professional fees etc.

2. Corporate Tax

-

- Levied on profits earned by corporates

- Since a company is a separate entity from an individual

- Present rate of corporate tax: 25 percent for turnover or revenue upto Rs 250 crore and above that – 30 percent

3. Dividend Distribution Tax (DDT)

-

- This has been abolished since 2020 as dividend income is now added to income of the receiver and income tax based on the slab is levied.

4. Security Transaction Tax (STT)

-

- On sale and purchase of securities on stock exchange

- Shares, bonds, ETFs, Mutual Funds etc

5. Professional Tax

-

- Unlike other direct taxes which are levied and collected by Centre, Professional Tax is levied and collected by the state governments.

- On salaries and professional fees.

- Presently states which impose professional tax are – Andhra Pradesh, Gujarat, Karnataka, Kerala, Maharashtra, Telangana, West Bengal

- Generally, a fixed tax of Rs 200 is imposed.

6. Minimum Alternate Tax (MAT)

-

- Imposed on zero-taxed companies

- MAT in income tax was introduced to ensure that even if a company reports substantial profits on its financial statements and utilises various exemptions and deductions during income tax e-filing to bring down its taxable income to zero or near-zero, it still contributes to the nation’s tax revenue.

- Current rate: 15 percent

7. Angel Tax

-

- Angel Tax is levied at 30 percent on net investments in startups in excess of the fair market value.

- It is considered as income from other sources for the start-ups.

How is it calculated?

For example, if a startup receives 50 crores of investment by issuing 1 lakh shares at Rs.5000 each to an Indian investor while the fair market value is Rs.2000 per share i.e. Rs.20 crore only, then the startup will have to pay angel tax on the amount more than the fair market value i.e. Rs. 30 crores. Therefore, Angel Tax payable in this transaction will be Rs. 9.27 crore (30.9% on Rs.30 crore).

8. Equalisation Levy

-

- It is a tax which is paid for digital services like:

- Online advertisement

- Provision for digital advertising space

- Any other facility or service for the purpose of online advertisement

- Current rate (2024) – 6 percent

- Equalisation Levy is a direct tax, which is withheld at the time of payment by the service recipient.

- It is a tax which is paid for digital services like:

B. Indirect Tax

-

- It is a tax whose impact and incidence fall on different persons.

- It is imposed mainly on the supply or sale of goods and services.

- It involves easy calculation as there are little exemptions and limited tax slabs

- E.g. – GST, Customs Duty

- An increase in indirect tax rate increases the cost of goods and services in the market which may lead to inflation.