Introduction:

Pradhan Mantri MUDRA Yojana (PMMY) Launched on 8 April 2015, has marked a decade of transformative impact under the vision of “Funding the Unfunded” by bridging the credit gap for millions of small entrepreneurs ranging from neighbourhood shopkeepers to small-scale manufacturers.

Key Points (As of April 2026)

-

- Massive Financial Outreach: Over 57 crore loans disbursed, amounting to a cumulative value of ₹40.07 lakh crore.

- Empowering New Voices: More than 12 crore accounts belong to first-time entrepreneurs.

- Inclusive Lending: Approximately 60% of loan accounts are held by women, and 45.52% belong to SC, ST, and OBC categories.

- Expanded Credit Limit: Collateral-free loans now available up to ₹20 lakh across four distinct categories.

Driving Credit to the Last Mile

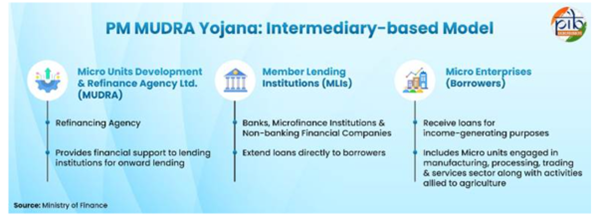

PMMY operates through a three-tier institutional framework designed to ensure seamless credit flow to the micro-enterprise sector.

-

- MUDRA Ltd (Refinancer): Acts as the apex supporting institution. In FY 2024-25, it reported its highest-ever profit of over ₹827 crore.

- Member Lending Institutions (MLIs): Includes Scheduled Commercial Banks, RRBs, Small Finance Banks, NBFCs, and MFIs responsible for direct last-mile delivery.

- Beneficiaries: Micro-enterprises engaged in manufacturing, trading, services, and agri-allied non-farm activities.

Supporting Enterprises: The Four Loan Categories

To cater to different stages of business growth, PMMY provides graded financial support.

| Category | Loan Limit | Target Group |

|---|---|---|

| Shishu | Up to ₹50,000 | Early-stage businesses and individuals with no credit history. |

| Kishor | ₹50,001 to ₹5 Lakh | Established units requiring funds for stabilization or modest expansion. |

| Tarun | ₹5 Lakh to ₹10 Lakh | Growing enterprises seeking to scale up operations and capacity. |

| Tarun Plus | ₹10 Lakh to ₹20 Lakh | High-performing borrowers with a stable track record of repaying Tarun loans. |

Strengthening the Framework

The integration of digital technology has enhanced the transparency and accessibility of Mudra loans.

-

- JanSamarth Portal: A unified digital gateway covering 14 credit-linked schemes and 200+ lenders to reduce administrative hurdles.

- CGFMU (Credit Guarantee): Administered by NCGTC, this fund provides guarantee cover, reducing credit risk for banks and facilitating collateral-free lending.

- MUDRA Cards: Facilitate working capital requirements through a digitized transaction model.

Case Studies

The true impact of PMMY is seen in the individual journeys of the “unfunded” becoming successful entrepreneurs.

-

- Poonam Kumari (Bihar): A farmer’s daughter-in-law who used an ₹8 lakh MUDRA loan to launch a seed trading business. Her monthly earnings have now reached ₹60,000, providing her with financial independence and family trust.

- Mudassir Naqshbandi (Kashmir): Transitioned from a job-seeker to a job-creator by using a MUDRA loan to build a thriving bakery in Baramulla. He now employs 42 people and handles transactions primarily through UPI, showcasing digital inclusion.

Challenges

Based on industry analysis and recent economic observations (2025-26):

-

- Asset Quality Concerns: The Hindu reports that as loan limits increase to ₹20 lakh (Tarun Plus), maintaining low Non-Performing Asset (NPA) levels remains a priority for lending institutions.

- Sustainability vs. Consumption: ORF notes that while credit access is high, a segment of “Shishu” borrowers still struggles to transition from subsistence-level activity to scalable growth.

- Digital Literacy: Indian Express highlights that in remote pockets, despite the JanSamarth portal, manual assistance is still heavily required for first-time entrepreneurs to navigate digital applications.

Way Forward

-

- Growth-Oriented Financing: Shifting focus from mere disbursement to ensuring the long-term sustainability of micro-enterprises through mentorship and market linkages.

- Enhanced Credit Scoring: Utilizing AI-driven digital footprints on portals like JanSamarth to provide more accurate credit assessments for borrowers without traditional collateral.

- Graduation Model: Encouraging “Kishor” and “Tarun” borrowers to transition into formal MSMEs that contribute significantly to regional industrial corridors.

Conclusion

By pairing digital public infrastructure with trust-based lending, the scheme has not only “funded the unfunded” but also fostered a new generation of job creators.

Spread the Word