THE INTRODUCTION: The need for a strong and resilient social infrastructure became even more important during the ongoing COVID-19 pandemic that brought into focus the vulnerabilities in social infrastructure across countries. Specifically, the pandemics posed the challenge of balancing livelihoods while saving lives. To save lives and livelihoods amidst the COVID crisis, countries have adopted various strategies. India, the country with the second-largest population and a large elderly population, adopted a multi-pronged approach. The government’s response through ‘Aatmanirbhar Bharat Abhiyan’ packages and other sector-specific initiatives have provided the necessary support to mitigate the adverse impact of a pandemic. This chapter gives a brief account of India’s response to Social Infrastructure and Employment.

INDIA’S HEALTH RESPONSE TO THE COVID-19

Like most other countries, India also faced two COVID-19 waves: the first in 2020 and the second in 2021. To save lives, the Government adopted a multi-pronged approach viz.

- Restrictions/partial lockdowns,

- Building capacity in health infrastructure,

- COVID-19 appropriate behavior, testing, tracing, treatment

- Vaccination drive.

COVID VACCINATION STRATEGY

- Guided by scientific and epidemiological evidence, World Health Organisation (WHO) guidelines, and global best practices, India’s National COVID Vaccination Program has been one of the world’s largest vaccination programs.

- Government of India procured 75 percent of monthly vaccine production and provided it free to States and UTs, while the rest could be procured by private hospitals.

- Availability of Vaccine: The ICMR funded the clinical trials of the COVISHIELD vaccine developed in collaboration with Oxford – Astra Zeneca. COVISHIELD and COVAXIN have been widely used vaccines in India. Every month about 250- 275 million doses of COVISHIELD and 50-60 million doses of COVAXIN have been produced.

- Pricing and equity: At all Government COVID-19 Vaccination Centres (CVCs), the COVID-19 vaccine was made available free of cost for all eligible citizens.

- Coverage: From 1st May 2021, all 94 crore persons of age 18 years and above, were made eligible for COVID vaccination. From 3rd January 2022, COVID-19 vaccine coverage has been extended to the age group of 15-18 years. Till 19th January 2022, 3.73 crore youngsters between 15-18 age group have been vaccinated with 1st dose of COVID-19 vaccine covering more than 50 percent of youngsters.

- Vaccine hesitancy: To reduce vaccine hesitancy, the Government made efforts that include awareness by identified experts. From 3rd November 2021, a campaign, ‘Har Ghar Dastak’, has been initiated to identify and vaccinate those who missed 1st dose and are due for 2nd dose through house-to-house mobilization activity.

- Technology-driven: Arogya Setu mobile app was launched to enable people to assess the risk of their catching the COVID-19 infection.

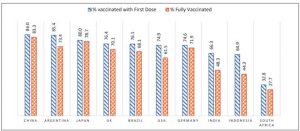

- Vaccination Progress: As of 16th January 2022, a total of 156.76 crore doses of COVID-19 vaccines have been administered: 90.75 crores first dose and 65.58 crores second dose.

Population vaccinated by country (in percent)

TRENDS IN SOCIAL SECTOR EXPENDITURE

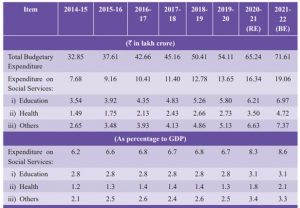

- Government’s spending on social services increased significantly during the pandemic. In 2021-22 (BE), Centre and State governments earmarked an aggregate of ` 71.61 lakh crore for spending on the social service sector; an increase of 9.8 percent over 2020-21.

- Last year’s (2020-21) revised expenditure has also gone up by ` 54,000 crores from the budgeted amount. In 2021-22 (BE), funds to the sector increased to 8.6 percent of Gross Domestic Product (GDP) (8.3 percent in 2020-21).

- During the last five years, social services accounted for about 25 percent of the total Government expenditure (Centre and States taken together). In 2021-22 (BE), it was 26.6 percent.

- Expenditure in the health sector increased from ` 2.73 lakh crore in 2019-20 (pre-COVID-19) to ` 4.72 lakh crore in 2021-22 (BE), an increase of nearly 73 percent.

- Union Budget 2021-22, announced Ayushman Bharat Health Infrastructure Mission, a new Centrally Sponsored Scheme, with an outlay of about ` 64,180 crores in the next five years to develop capacities of primary, secondary, and tertiary care Health Systems

- Union Budget 2021-22 provided an outlay of Rs 35,000 crore towards COVID-19 vaccination.

- The National Health Policy, 2017 envisaged increasing the government’s health expenditure to 2.5 percent of GDP by 2025.

EDUCATION

- During initial COVID-19 restrictions, as a precautionary measure to protect the students from COVID-19, schools, and colleges were closed across India. This posed a new challenge for the Government in terms of continuity of education.

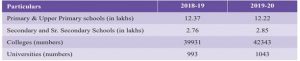

- School Infrastructure An assessment for the pre-pandemic year of 2019-20 for which data is available reveals that the number of recognized schools & colleges continued to increase between 2018-19 and 2019-20, except for primary & upper primary schools.

SCHOOL INFRASTRUCTURE

- An assessment for the pre-pandemic year of 2019-20 for which data is available reveals that the number of recognized schools & colleges continued to increase between 2018-19 and 2019-20, except for primary & upper primary schools.

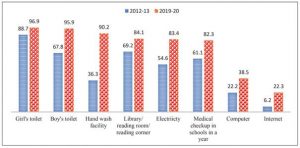

- Toilets (girls or boys), drinking water, and hand-washing facilities are now available in most Government schools (10.32 lakh).

- Priority to drinking water and sanitation in schools under Jal Jeevan Mission, Swachh Bharat Mission as well as under Samagra Shiksha Scheme has been instrumental in providing required resources and creating these assets in schools.

- As of 19.01.2022, under Jal Jeevan Mission 8,39,443 schools were provided a tap water supply.

- Availability of teachers, measured by Pupil-Teacher Ratio, an indicator whose decrease signals improvement in quality of education, has improved at all levels continuously from 2012-13 to 2019-20: from 34 to 26 at primary, 23 to 18 at upper primary, 30 to 18 at secondary, and 39 to 26 at the higher secondary level.

Schools with Basic Facilities

SCHOOL ENROLMENT

- In 2019-20, 26.45 crore children were enrolled in schools. During the year, schools enrolled about 42 lakh, additional children, out of which 26 lakh were in primary to higher secondary levels and 16 lakh were in pre-primary as per the Unified District Information System for Education plus (UDISE+) database.

- The enrollments increased across all levels viz., upper-primary, secondary, and higher secondary, except for the primary level. At the primary level, enrollment reduced from 13.5 crores in 2012-13 to 12.2 crores in 2019-20. This decline in enrollment was because of a decline in the total number of children in the age group 6-10 years.

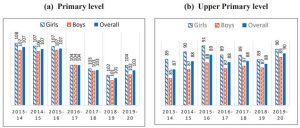

School Gross Enrollment Ratios in India (in percent)

SCHOOL DROP-OUT

- the years 2019-20 saw a decline in dropout rates at primary, upper-primary, and secondary levels. In 2019-20, the school dropout rate at the primary level declined to 1.45 percent from 4.45 percent in 2018-19.

- ASER found that despite the pandemic, enrollment in the age cohort of 15-16 years continued to improve as the number of not enrolled children in this age group declined from 12.1 percent in 2018 to 6.6 percent in 2021.

Major Initiatives for Students during the COVID-19 pandemic

PM e-VIDYA: Major components

- One Nation, One Digital Education (DIKSHA) Platform

- One Class, One TV channel through Swayam Prabha TV Channels

- Extensive use of Radio, Community Radio, and Podcasts

- One DTH channel is being operated specifically for hearing impaired students in sign language.

National Digital Education Architecture (NDEAR): A digital infrastructure for Education, was launched on 29th July 2021.

Vidyanjali: To connect the Government and Government aided schools through a community/ volunteer management program.

Major Schemes for School Education during 2021-22

- Samagra Shiksha Scheme has been continued for a period of five years, from 2021-22 to 2025-26.

- NIPUN Bharat Mission: On 5th July 2021, the government launched a National Mission on Foundational Literacy and Numeracy called “National Initiative for Proficiency in Reading with Understanding and Numeracy (NIPUN Bharat)”.

- Pradhan Mantri Poshan Shakti Nirman (PM POSHAN) Scheme: The Scheme, earlier known as the ‘National Programme for Mid-Day Meal in Schools”, covers all school children studying in Balvatika (just before class I) and Classes I-VIII in Government and Government-Aided Schools.

HIGHER EDUCATION

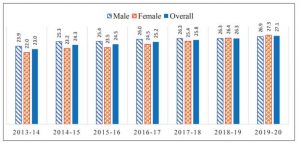

- Gross enrollment ratio in higher education was recorded at 27.1 percent in 2019-20, slightly higher than 26.3 percent in 2018-19. For males, it has also increased from 26.3 percent in 2018-19 to 26.9 percent in 2019-20 while for females it has increased from 26.4 percent to 27.3 percent respectively.

Gross Enrollment Ratios in Higher Education for age 18-23 years (in percent)

SKILL DEVELOPMENT

- To unlock the demographic dividend, several steps have been taken to increase the skill levels in the population. Periodic Labour Force Survey (PLFS) 2019-20 shows that formal vocational/technical training among youth (age 15-29 years) and working population (age 15-59 years) have improved in 2019-20 over 2018-19.

- The improvement in skills has also been for males and females, both in rural and urban sectors. However, formal training for males and females is lower in rural than in urban areas.

- As per the report of the first quarter (April-June, 2021) of the Quarterly Employment Survey (QES) in respect of establishments employing at least 10 workers in major nine sectors, 17.9 percent of estimated establishments were imparting formal skill training.

SKILL INDIA MISSION

- Launched in 2015, Skill India Mission focuses on re-skilling and up-skilling in prominent trades. Under the Mission, the government implements Pradhan Mantri Kaushal Vikas Yojana (PMKVY), Jan Shikshan Sansthan (JSS) Scheme, and National Apprenticeship Promotion Scheme (NAPS), for providing short term Skill Development training and Craftsman Training Scheme (CTS), for long term training, to the youth.

Pradhan Mantri Kaushal Vikas Yojana (PMKVY)

- PMKVY has two training components, viz., Short Term Training (STT) and Recognition of Prior Learning (RPL). Between 2016-17 and 2021-22 (as of 15 January 2022 ), under PMKVY 2.0 about 1.10 crore persons were trained (inclusive of the placement-linked and non-placement-linked components of the PMKVY).

Jan Shikshan Sansthan (JSS) Scheme

- JSS aims to provide vocational skills to non-literate, neo-literates, persons with a rudimentary level of education up to 8th and school dropouts up to 12th standard in the age group of 15-45 years. The priority groups are women, SC, ST, minorities, Divya Gyan, and other backward sections of the society.

National Apprenticeship Promotion Scheme (NAPS)

- This Scheme promotes apprenticeship training and the engagement of apprentices by providing financial support to industrial establishments undertaking apprenticeship programs under The Apprentices Act, 1961. As of 31 October 2021, 4.3 lakh apprentices are engaged under the scheme.

Craftsmen Training Scheme (CTS)

- CTS is for providing long-term training in 137 trades through 14,604 Industrial Training Institutes (ITIs) across the country. For session 2020, 13.36 lakh trainees were enrolled.

TRENDS OF EMPLOYMENT

In the absence of high-frequency data on labour market indicators, other proxies such as subscriptions to the EPFO scheme and demand for work under MGNREGA, have been used to analyze the more recent trends in employment in urban and rural sectors.

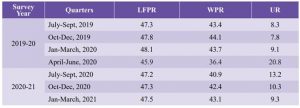

Trends in Urban employment using Quarterly PLFS data

- In the first quarter of 2020-21, the unemployment rate for the urban sector rose to 20.8 percent. The LFPR and WPR in the urban sector also declined significantly during this quarter.

- The UR gradually declined during this period to reach 9.3 percent in Q4 of 2020-21. The UR for males as well as females, aged 15 & above, recovered to the pre-pandemic levels.

TRENDS IN DATA ON DEMAND FOR WORK UNDER MGNREGS

- During the nationwide lockdown, the aggregate demand for MGNREGS work peaked in June 2020, and has thereafter stabilized.

- During the second COVID wave, demand for MGNREGS employment reached the maximum level of 4.59 crore persons in June 2021. Nonetheless, after accounting for seasonality, the demand at an aggregate level still seems to be above the pre-pandemic levels of 2019.

- For some states like Andhra Pradesh and Bihar, the demand for work under MGNREGS has reduced to below the pre-pandemic levels during the last few months.

- Intuitively, one may expect that higher MGNREGS demand may be directly related to the movement of migrant labouri. e. source states would be more impacted. Nevertheless, state-level analysis shows that for many migrant source states like West Bengal, Madhya Pradesh, Odisha, Bihar, the MGNREGS employment in most months of 2021 has been slower than the corresponding levels in 2020.

- In contrast, the demand for MGNREGS employment has been higher for migrant recipient states like Punjab, Maharashtra, Karnataka, and Tamil Nadu for most months in 2021 over 2020.

Long-term trends in employment using annual PLFS data

- During the Periodic Labour Force Survey (PLFS) 2019-20 (survey period from July 2019 to June 2020), employment at its usual status continued to expand. Between 2018-19 and 2019-20, about 4.75 crore additional persons joined the workforce.

- This is about three times more than the employment created between 2017-18 and 2018-19.

POLICY RESPONSES TO BOOST RURAL LIVELIHOOD

Incentives for job creation: Aatmanirbhar Bharat Rojgar Yojana (ABRY) was announced as a part of the Aatmanirbhar Bharat 3.0 package to boost the economy, increase the employment generation in the post-Covid recovery phase, and incentivize the creation of new employment along with social security benefits and restoration of loss of employment during COVID-19 pandemic.

Wage employment: To boost employment and livelihood opportunities for returnee migrant workers, Garib Kalyan Rojgar Abhiyaan was launched in June 2020. It focused on 25 target-driven works to provide employment and create infrastructure in the rural areas of 116 districts of 6 States with a resource envelope of Rs 50,000 crore.

Boosting Self-employment:

- The program targets to mobilize about 9-10 crore households into Self Help Groups (SHGs).

- Till December 2021, 8.07 crore households are mobilized into SHGs.

Social protection:

- Pradhan Mantri Shram Yogi Maan-Dhan (PM-SYM) Yojana, launched on 05.03.2019, is a voluntary and contributory pension scheme for providing a monthly minimum assured pension of ` 3000 upon attaining the age of 60 years.

- As of 17.01.2022, the enrollment under the PMSYM scheme is 46.09 lakh persons, out of which female enrollment was 23.89 lakh and male enrollment was 22.20 lakh.

e-SHRAM Portal

- e-SHRAM portal has been launched to create a National Database of Unorganized Workers (UWs). One of the main objectives of this portal is to facilitate the delivery of Social Security Schemes to the workers. This database is seeded with Aadhaar and for the age group between 16-59 years.

- It includes construction workers, migrant workers, gig workers, platform workers, agricultural workers, MGNREGA workers, fishermen, milkmen, ASHA workers, Anganwadi workers, street vendors, domestic workers, rickshaws pullers, and other workers engaged in similar other occupations in the unorganized sector.

Status of Labour Reforms

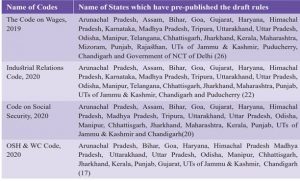

- In 2019 and 2020, 29 Central Labour laws were amalgamated, rationalized, and simplified into four labor codes, viz., the Code on Wages, 2019 (August 2019), the Industrial Relations Code, 2020, the Code on Social Security, 2020, and the Occupational Safety, Health & Working Conditions Code, 2020 (September 2020).

- The new laws were in tune with the changing labour market trends and at the same time accommodated the minimum wage requirement and welfare needs of the unorganized sector workers.

HEALTH

PROGRAMMES AND SCHEMES FOR THE HEALTH SECTOR

- Ayushman Bharat Health and Wellness Centres (AB-HWCs): The vision of Ayushman Bharat is to achieve universal health coverage. It adopts a continuum of care approach, comprising two inter-related components. The first component is the creation of 1,50,000 Health and Wellness Centres (HWCs) which cover both, maternal and child health services and non-communicable diseases, including free essential drugs and diagnostic services.

- Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY): The scheme provides a health cover of ` 5 lakhs per family per year for secondary and tertiary care hospitalization to over 10.74 crores of poor and vulnerable families in the bottom 40 percent of the Indian population.

- PM-Ayushman Bharat Health Infrastructure Mission (PM-ABHIM) is a mission to develop the capacities of primary, secondary, and tertiary care health systems, strengthen existing national institutions, and create new institutions, to cater to the detection and cure of new and emerging diseases. It is the largest pan-India scheme for public health infrastructure since 2005.

- Pradhan Mantri Swasthya Suraksha Yojana (PMSSY) is being implemented to correct regional imbalances in the availability of affordable reliable tertiary healthcare services and to augment facilities for quality medical education in the country.

- Ayushman Bharat Digital Mission (ABDM), erstwhile National Digital Health Mission (NDHM), announced on 27th September 2021 to develop the backbone necessary to support the integrated digital health infrastructure of the country.

- e-Sanjeevani: In wake of the COVID-19 pandemic, the Ministry of Health and Family Welfare upgraded the thee-Sanjeevani application to enable patient-to-doctor teleconsultation to ensure a continuum of care and facilitate health services to all citizens in the confine of their homes free of cost.

HEALTH OUTCOME INDICATORS

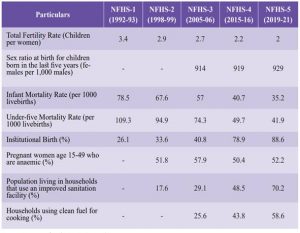

As per the latest National Family Health Survey (NFHS)-5, social indicators such as total fertility rate, sex ratio, and health outcome indicators viz., infant mortality rate, under-five mortality rate, institutional birth rates have improved over the year 2015-16.

CHILD HEALTH INDICATORS

- All child nutrition indicators have also improved at all Indian levels. Under Five Mortality Rate (U5MR) has declined from 49.7 in 2015-16 to 41.9 in 2019-21. Infant Mortality Rate (IMR) has declined from 40.7 per 1000 live births in 2015-16 to 35.2 per 1000 live births in 2019-21.

- Stunting has declined from 38 percent in 2015-16 to 36 percent in 2019-21. Wasting has also declined from 21 percent in 2015-16 to 19 percent in 2019-21. And, underweight declined from 36 percent in 2015-16 to 32 percent in 2019-21.

LIFE EXPECTANCY

- Life expectancy at birth was 69.4 years for the period 2014-18; it has increased by 0.4 years from 2013-17. It varies widely across states; ranging from the lowest at 65.2 years in Chhattisgarh to the highest at 75.3 years in Kerala and Delhi. It is higher in urban areas (72.6 years) than in rural areas (68.0 years).

DRINKING WATER AND SANITATION

JAL JEEVAN MISSION (JJM)

- In 2019, out of about 18.93 crore families in rural areas, about 3.23 crore (17 percent) rural families had tap water connections in their homes. As of 2 January 2022, 5,51,93,885 households have been provided with a tap water supply since the start of the mission.

- Six states/ Uts have achieved the coveted status of 100 percent households with tap water supply, namely Goa, Telangana, A & N Islands, Puducherry, Dadra, Nagar Haveli, Daman and Diu, and Haryana.

SWACHH BHARAT MISSION (GRAMEEN) [SBM-G]

- During 2021-22 (as of 25.10.2021) a total of 7.16 lakh Individual household latrines for new emerging households and 19,061 Community Sanitary Complexes have been constructed. Also, 2,194 villages have been declared as ODF Plus.

- As per the recently released findings of the fifth round of the National Family Health Survey, 2019-21 (NFHS-5), the population living in households that use an improved sanitation facility has increased from 48.5 percent in 2015-16 to 70.2 percent in 2019-21.

ELECTRICITY AND CLEAN COOKING FUEL

- As per NFHS-5, 58.6 percent of households were using clean fuel for cooking in 2019-21, a significant increase from 43.8 percent in 2015-16.

RURAL DEVELOPMENT

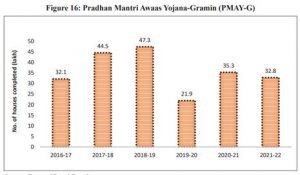

PRADHAN MANTRI AWAAS YOJANA-GRAMIN (PMAY-G)

- In the first phase from 2016-17 to 2018-19, one crore houses were taken up. Under phase II, assistance is being provided for the construction of the remaining 1.95 crore houses from 2019-20 to 2021-22.

- As of 18th January 2022, 2.17 crore houses have been sanctioned and 1.69 crore houses completed against a target of 2.63 crore houses till 2021-22.

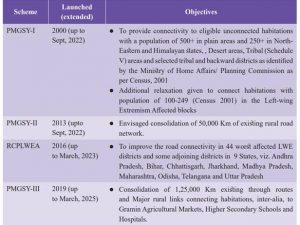

PRADHAN MANTRI GRAM SADAK YOJANA (PMGSY)

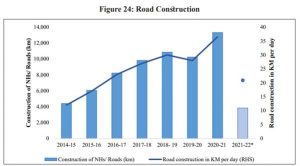

- As of 18.01.2022, a total of 1,82,506 roads measuring 7,82,844 km and 9,456 Long Span Bridges (LSBs) have been sanctioned and 1,66,798 roads measuring 6,84,994 km and 6,404 LSBs have been completed.

- World Bank (2019) in an evaluation of the scheme found that PMGSY roads had a positive impact on human capital formation in rural India.

MULTIDIMENSIONAL POVERTY (MPI)

- Using the NFHS-4 (2015-16) report, in line with the global Multidimensional Poverty Index (MPI), NITI Aayog prepared Multidimensional Poverty Index at the national, for all states and districts of India.

- It will enable measuring deprivation across twelve indicators at the national, state, and districts level. In 2015-16, 25 percent of households were found to be multidimensional poor in India.

- Among states, Bihar had the largest (51.91%) multidimensional poor households, followed by Jharkhand (42.16%), Uttar Pradesh (37.79%), Madhya Pradesh (36.65%), Assam (32.67%), and Rajasthan (39.46%).

- Since the MPI index is based on NFHS-4 data of 2014-15, it may serve as the baseline for measuring deprivation in future studies.